The Machine - How Money Actually Circulates

You earn money. You spend money. You save money. And in between earning and spending, money moves. It moves through your bank account. Through payment systems. Through the accounts of businesses, governments, and other people. It circulates. And the circulation is not random. It follows pathways. Structured pathways. Pathways built by institutions, regulated by rules, and powered by incentives that most people never see.

This is the money system. And it is not what you think it is. Because when most people think about money, they think about cash. Notes and coins. Physical objects you hold in your hand. But cash is a tiny fraction of the money that exists. The vast majority of money is digital. Numbers in accounts. And those numbers move through a system that is far more complex, far more concentrated, and far more powerful than the physical cash in your wallet suggests.

Let me show you how the machine actually works.

The first thing to understand is that most money is not created by governments. Governments print cash. But cash is not where most money comes from. Most money is created by commercial banks. And they create it through lending.

Here is how it works. You go to a bank and ask for a loan. Let us say you want to borrow ten thousand pounds. The bank does not go to a vault, take out ten thousand pounds in cash, and hand it to you. The bank does not take ten thousand pounds from someone else's account and transfer it to yours. The bank creates the money. It credits your account with ten thousand pounds. And in that moment, that money comes into existence. It did not exist before. Now it does.

This is called credit creation. And it is how the majority of money in the economy is made. Not by central banks. Not by governments. By commercial banks making loans. Every time a bank lends, it creates money. And every time a borrower repays, that money is destroyed. The money supply is not fixed. It expands and contracts based on how much lending is happening.

Now, this does not mean banks can create infinite money. They are constrained. But the constraints are not what most people think. The constraint is not that banks need to have the money before they lend it. The constraint is capital requirements. Banks are required to hold a certain amount of capital, a cushion, relative to the loans they make. If they lend more, they need more capital. But the capital required is a fraction of the loan. So a bank with one million pounds in capital can lend far more than one million pounds. This is called fractional reserve banking. And it is why banks are so powerful. They multiply money.

But they do not do it alone. They do it within a system. And the system has a center. The central bank.

The central bank is not like a commercial bank. It does not serve customers. It does not take deposits from you or lend to you. It serves the banking system. It is the bank for banks. And it has two main jobs. One, manage the supply of money. Two, act as a lender of last resort.

Managing the money supply happens through interest rates. The central bank sets a rate, called the base rate or the policy rate, which influences the rates that commercial banks charge when they lend. If the central bank raises its rate, borrowing becomes more expensive. People and businesses borrow less. Less borrowing means less money creation. The money supply grows more slowly. If the central bank lowers its rate, borrowing becomes cheaper. More people borrow. More money is created. The money supply expands.

This is how central banks try to control inflation and manage the economy. Raise rates to cool things down. Lower rates to stimulate. But the central bank does not control the money supply directly. It influences it. Through the price of borrowing. And that influence depends on commercial banks and borrowers responding the way the central bank expects. Which they do not always do.

The second role of the central bank is to act as a lender of last resort. If a commercial bank runs into trouble, if it cannot meet its obligations, it can borrow from the central bank. This prevents bank runs. It prevents the collapse of individual banks from triggering a collapse of the entire system. The central bank stands behind the commercial banks. And that backing is what makes people trust that their deposits are safe. Even though, as we have established, the banks do not actually have all the money. They have a fraction. The rest is lent out. Or rather, created through lending.

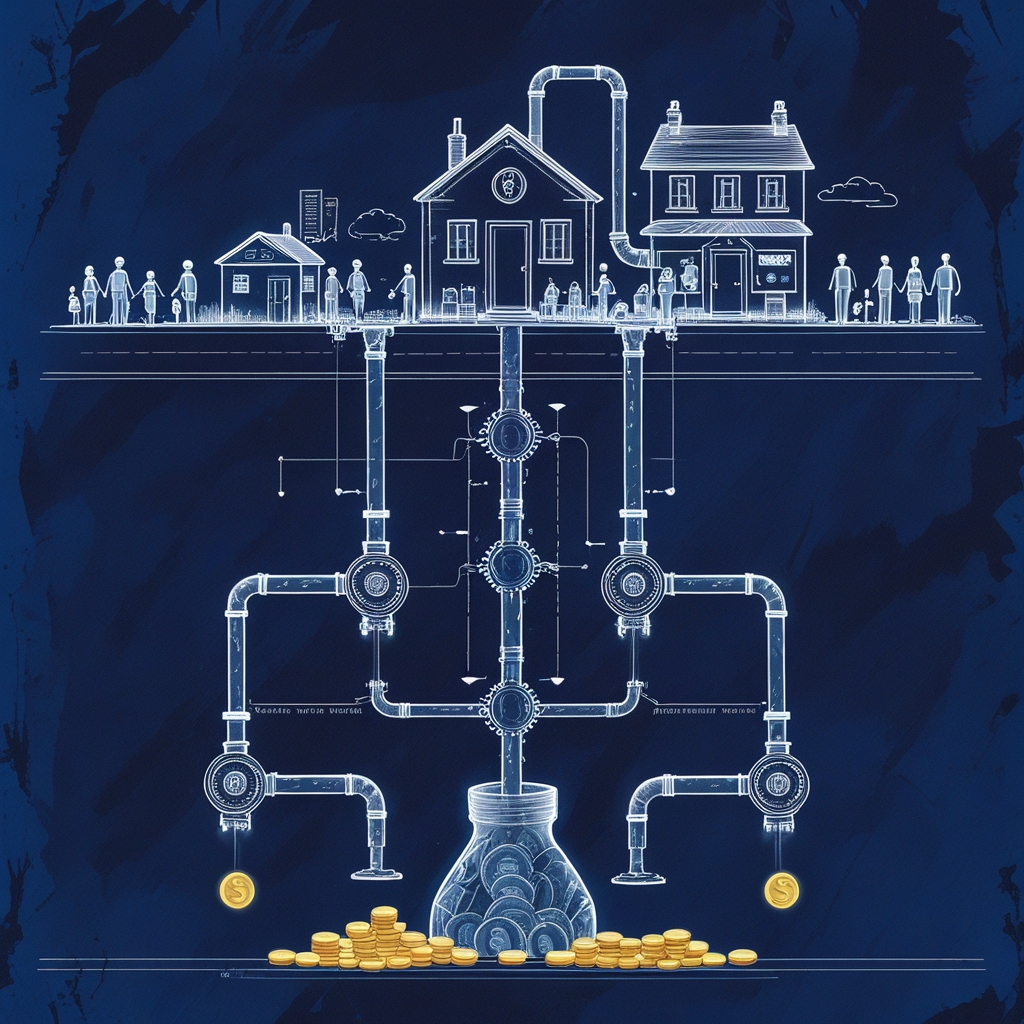

Now let us talk about how money moves. Because money does not just sit in accounts. It circulates. And the circulation happens through payment systems.

When you pay for something with a debit card, you are not handing over physical money. You are instructing your bank to transfer a number from your account to the account of the business you are paying. That instruction goes through a payment network. The network checks that you have the money. It authorizes the transaction. And it settles the transaction by adjusting the balances in the relevant accounts. Your balance goes down. The business's balance goes up. The money has moved. Digitally.

Most of these transactions happen within the same country. And they are settled through domestic payment systems. In the UK, systems like Faster Payments or BACS handle this. In the US, it is systems like ACH or Fedwire. These systems are the plumbing. Invisible to most people. But essential. Because without them, digital money cannot move.

For international payments, the system is more complex. If you want to send money to someone in another country, your bank and their bank are probably not part of the same payment network. So the payment has to go through intermediaries. Correspondent banks. Banks that have accounts with each other and facilitate the transfer. The instruction goes from your bank to a correspondent bank. The correspondent bank communicates with the recipient's bank. The balances are adjusted. The money moves.

This is slow. And expensive. Because every intermediary takes a fee. And because the process involves multiple steps, each of which introduces delay. International payments can take days. And the fees can be significant. Especially for small amounts. This is why remittances, money sent by workers in one country to family in another, are so costly. The system is not designed for small, cross-border payments. It is designed for large, institutional transactions. And individuals bear the cost of that design.

Now let us talk about foreign exchange. Because money exists in different currencies. And currencies have different values. If you want to send pounds to someone who uses dollars, the pounds have to be converted. And conversion happens in foreign exchange markets.

Foreign exchange markets are where currencies are traded. Banks, businesses, investors, governments, all of them buy and sell currencies. And the price, the exchange rate, is determined by supply and demand. If more people want pounds, the price of pounds goes up. If more people want dollars, the price of dollars goes up. The exchange rate fluctuates constantly. And those fluctuations matter. Because they affect the cost of imports, the value of exports, the returns on investments, the price of everything that crosses borders.

Central banks sometimes intervene in foreign exchange markets. If they think their currency is too strong or too weak, they buy or sell it to influence the price. But intervention only works if the market believes the central bank has the resources and the commitment to sustain it. And most of the time, the market is bigger than the central bank. So intervention is limited.

Now, all of this, the creation of money by commercial banks, the management of the money supply by the central bank, the movement of money through payment systems, the conversion of money through foreign exchange markets, all of this happens within a structure of rules. And the rules are set by governments and regulators.

Banks are required to hold capital. They are required to maintain liquidity, enough cash or cash-like assets to meet withdrawals. They are required to report their activities. They are subject to stress tests, simulations of what would happen in a crisis. And they are supervised by regulators who are supposed to ensure they are not taking excessive risks.

But the rules are not static. They change. After every crisis, they tighten. And then, over time, they loosen. Because the memory of the crisis fades. Because banks lobby for relief. Because regulators are influenced by the industry they regulate. The cycle repeats. Tighten after the crash. Loosen during the boom. And the next crash reveals that the loosening went too far.

So here is what the money system looks like. A network of commercial banks creating money through lending. A central bank managing the supply and acting as a backstop. Payment systems moving money domestically and internationally. Foreign exchange markets converting money between currencies. And a regulatory framework trying, with limited success, to keep the system stable.

This is the machine. And it is not neutral. It is not just a tool for facilitating transactions. It is a structure that concentrates power. Because the ability to create money is the ability to decide who gets access to resources. And that ability is held by a small number of institutions. Commercial banks decide who gets loans. Central banks decide the price of borrowing. Payment networks decide how money moves. And all of these decisions shape the economy. They shape who prospers and who does not. They shape what gets built and what does not. They shape the future.

And the people making these decisions are not elected. They are not accountable to the public in the way governments are. They operate within rules. But the rules are written in ways that leave significant discretion. And that discretion is exercised in ways that reflect the interests and assumptions of the people exercising it.

The next article will show you who profits from this system. Because the system is not just a machine for moving money. It is a machine for extracting value. And the extraction happens at every point where money changes hands. Through interest. Through fees. Through currency conversion spreads. Through the advantage of being inside the system rather than outside it. The machine works. But it works for some people far more than it works for others.

And understanding who benefits, and how, is the key to understanding why the system is the way it is. Because the system is not an accident. It is a design. And the design reflects the priorities of the people who built it.